.png?width=292&height=292&name=Copy%20Link%20(1).png)

SIGN UP FOR FREE NEWSLETTER

SIGN UP FOR FREE NEWSLETTER

We’re all feeling the pinch these days, with the soaring cost of living and the recent round of interest rate hikes placing stress on the household budget. So any method that might relieve the financial squeeze is a welcome one - especially a strategy geared at reducing home loan interest costs.

And that’s exactly what an offset account can do. It’s a term most people are familiar with, but few understand.

So, what is an offset account and should you use one?

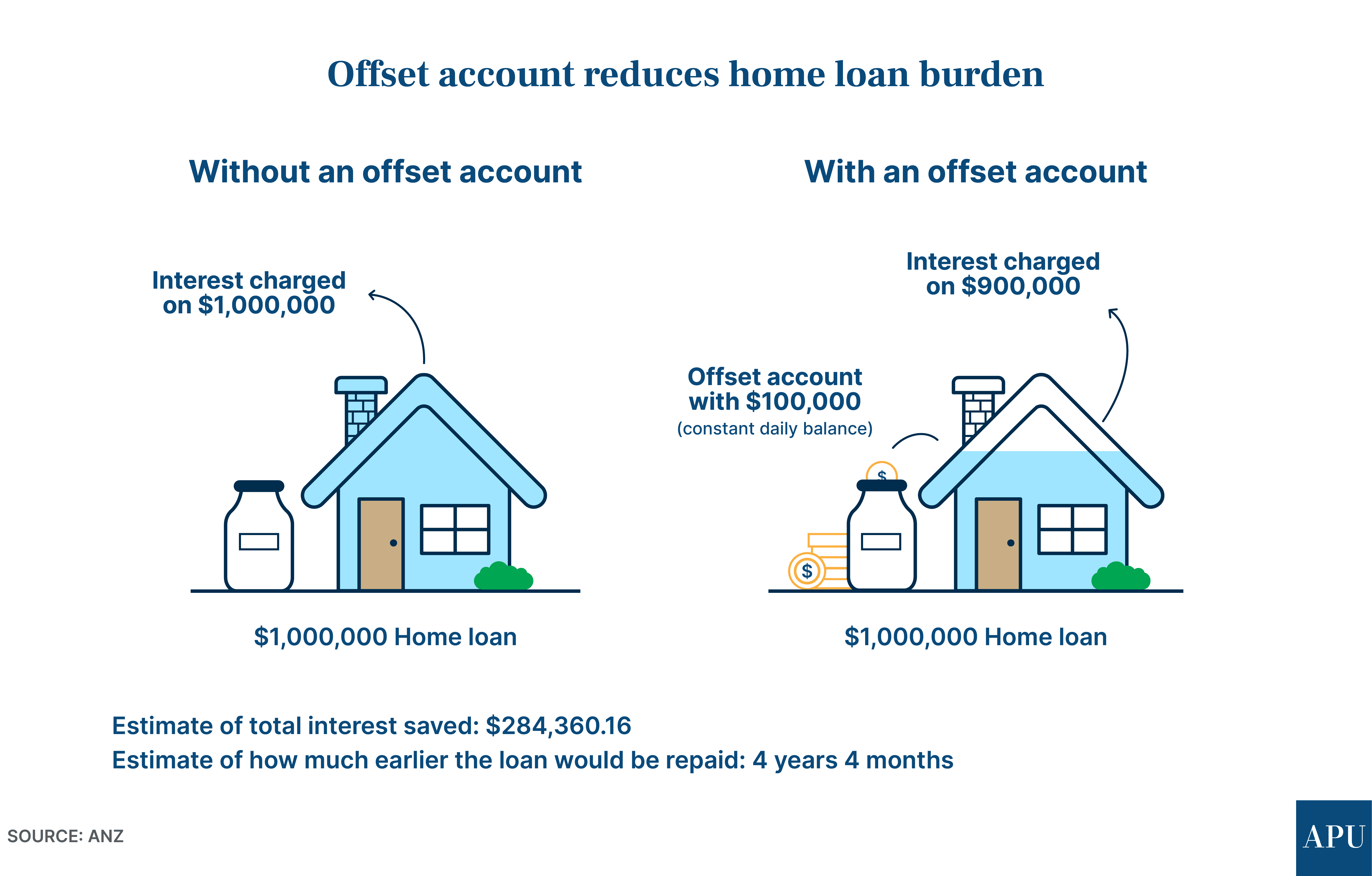

Fundamentally, an offset account is a bank account linked to a home loan, in which any funds held are used to offset the interest on the mortgage.

For example, if you have a $1 million home loan and $100,000 in your offset account, you will only be charged interest on $900,000 of the home loan.

Over the life of the loan, the savings can add up, potentially shaving years off the time it takes to pay off a home loan. However, discipline and large amounts of savings are required, and there are a range of other factors to consider before diving into this strategy.

The prospect of avoiding paying interest sounds extremely compelling, and the figures do sell a strong case for an offset account.

How much could you save?

Westpac’s calculator suggests that, based on a loan balance of $500,000 and a lifetime of 30 years, an offset account with an initial deposit of $40,000 and monthly deposits of $300 could save the account holder $359,824 in interest, shaving 8 years and 6 months off the life of the loan. This calculation is based on a variable interest rate of 7.54 percent.

This calculation is also based on a full offset account, rather than a partial offset account. The difference between these two types is as the names suggest - a full offset account means that the interest is offset against all funds held in the account, whereas a partial offset account means that interest is only offset against a portion of what is held in the account.

Other features of an offset account generally include ATM access, online access, a debit card to access funds, and no minimum balance requirements.

With the basics of an offset account out of the way, the question remains - are they worth utilising as a part of your financial strategy? There’s no straight answer here, as everyone has individual circumstances to consider, but there are some clear benefits to using an offset account.

Benefits

Interest Savings: The primary advantage of an offset account is the potential to save on interest payments. By offsetting the balance of a home loan with funds held in an offset account, borrowers effectively reduce the amount on which interest is calculated, leading to significant savings over the life of the loan.

Flexibility: Offset accounts offer a level of flexibility not typically found in traditional re-draw structures. The funds in the offset account remain accessible to the account holder at any time, providing liquidity and financial security. Account holders are rarely subject to withdrawal fees, and funds are theirs to use as they like. But it must be noted that the lower the funds, the lesser savings in interest that can be made.

Tax Efficiency: Unlike traditional savings accounts, you won’t earn interest in an offset account, but rather save interest on your mortgage repayments instead. The interest saved by using an offset account is not subject to tax. This can be particularly advantageous for individuals in higher tax brackets, as it effectively boosts the after-tax return on savings.

Accelerated Debt Repayment: By leveraging the interest savings from an offset account, borrowers can expedite the repayment of their mortgage. By making additional contributions to the offset account, borrowers can further reduce the interest payable and shorten the loan term.

With that said, there are also considerations to make, as with any investment or financial strategy. Here are the potential downsides of using an offset account.

Drawbacks

Loan size: Offset accounts tend to be more advantageous for larger loan amounts. If you have a small mortgage, the potential interest savings may not justify the fees associated with maintaining an offset account.

Financial discipline: To fully capitalise on the benefits of an offset account, borrowers must exercise financial discipline. Regular contributions to the offset account are essential to maximise interest savings and accelerate debt repayment.

%20Scott%20Kuru%20DPU%20248.jpg?width=1920&height=1080&name=Major%20Banks%20CAUGHT%20Preparing%20For%20Australia%E2%80%99s%20Biggest%20Housing%20Crash%20(Defaults%20%26%20Bankruptcies%20Coming)%20Scott%20Kuru%20DPU%20248.jpg)

%20Scott%20Kuru%20DPU%20247.jpg?width=1920&height=1080&name=This%20Is%20How%20Australia%20Gets%20Pushed%20Into%20the%20Next%20Big%20Reset%20(Trust%20Collapse%20Has%20Officially%20Begun)%20Scott%20Kuru%20DPU%20247.jpg)

%20Scott%20Kuru%20DPU%20239.jpg?width=1920&height=1080&name=URGENT%20Life%20In%20Australia%20Has%20Become%20Impossible%20For%20Millions%20Of%20Aussies%20(It%E2%80%99s%20About%20To%20Get%20Worse)%20Scott%20Kuru%20DPU%20239.jpg)

%20Scott%20Kuru%20DPU%20227.jpg?width=1920&height=1080&name=URGENT%20ALERT%20Australia%E2%80%99s%20Property%20Market%20Is%20Sliding%20Into%20Something%20Much%20Bigger%20(Prepare%20Now)%20Scott%20Kuru%20DPU%20227.jpg)

%20Scott%20Kuru%20DPU%20221.jpg?width=1920&height=1080&name=The%20AI%20Situation%20in%20Australia%20Just%20Hit%20a%20Point%20of%20No%20Return...%20(Major%20Bank%20Proves%20It)%20Scott%20Kuru%20DPU%20221.jpg)

%20Scott%20Kuru%20DPU%20218.jpg?width=1920&height=1080&name=URGENT%20Australia%E2%80%99s%20Diesel%20Supply%20Is%20Far%20Worse%20Than%20People%20Realise%20(Major%20Bank%20Warns)%20Scott%20Kuru%20DPU%20218.jpg)

%20Scott%20Kuru%20DPU%20216.jpg?width=1920&height=1080&name=This%20Is%20How%20Recessions%20Start%20Aussies%20Are%20Shutting%20Their%20Wallets%20(Prepare%20Now)%20Scott%20Kuru%20DPU%20216.jpg)

%20Scott%20Kuru%20DPU%20213.jpg?width=1920&height=1080&name=BREAKING%20Australia%E2%80%99s%20Govt%20Just%20Got%20Caught%20(The%2047%25%20%E2%80%9CPartner%E2%80%9D%20Tax%20Grab)%20Scott%20Kuru%20DPU%20213.jpg)

%20Scott%20Kuru%20DPU%20203.jpg.jpg?width=1920&height=1080&name=Australia%E2%80%99s%20Housing%20Crisis%20Just%20Flipped%20Again%20(BIGGEST%20MARKET%20CRASH%20COMING)%20Scott%20Kuru%20DPU%20203.jpg.jpg)

%20Scott%20Kuru%20DPU%20200.jpg?width=1920&height=1080&name=The%20Govt%E2%80%99s%20Biggest%20Money%20Grab%20The%20Average%20Aussie%20Is%20Getting%20Crushed%20(And%20It%E2%80%99s%20Getting%20Worse)%20Scott%20Kuru%20DPU%20200.jpg)

%20Scott%20Kuru%20DPU%20198.jpg?width=1920&height=1080&name=Farmers%20Panic%20as%20Fuel%20Crisis%20Takes%20Over%20Australia%E2%80%99s%20Fertiliser%20Supply%20(Food%20Shock%20Has%20Begun)%20Scott%20Kuru%20DPU%20198.jpg)

%20Scott%20Kuru%20DPU%20197.jpg?width=1920&height=1080&name=URGENT%20Australia%E2%80%99s%20Property%20Market%20Is%20One%20Rate%20Hike%20Away%20From%20Snapping%20(This%20Is%20How%20It%20Starts)%20Scott%20Kuru%20DPU%20197.jpg)

%20Scott%20Kuru%20DPU%20195.jpg?width=1920&height=1080&name=The%20Biggest%20$83Bn%20Housing%20Scam%20Just%20Got%20Exposed%20(They%E2%80%99re%20Addicted%20to%20Taxing%20the%20Everyday%20Aussie)%20Scott%20Kuru%20DPU%20195.jpg)

%20Scott%20Kuru%20DPU%20192.jpg?width=1920&height=1080&name=The%20Middle%20Class%20Is%20Getting%20Wiped%20Out%20of%20Housing%20(Even%20When%20They%20Do%20Everything%20Right)%20Scott%20Kuru%20DPU%20192.jpg)