.png?width=292&height=292&name=Copy%20Link%20(1).png)

SIGN UP FOR FREE NEWSLETTER

SIGN UP FOR FREE NEWSLETTER

Over the last month or so, there’s been a noticeable shift in the expectations of many economists and market traders about an issue that’s of vital importance to Australians with a mortgage.

The shift centres around when the Board of the Reserve Bank of Australia (RBA) will begin cutting interest rates.

With rates at their highest point in 12 years, that can’t come soon enough for many—especially those who bought property when official interest rates were at emergency pandemic lows of 0.1% between November 2020 and May 2022.

The bad news is that there is now a view that any RBA cut may not come until 2025 at the earliest.

And while you may think that a high cash rate doesn’t bode well for property prices, think again.

Property prices have continued to rise faster this year than many had predicted, with CoreLogic’s national Home Value Index putting on a total of 1.6% growth in the first three months of this year alone.

If those results continue to be replicated, Australia is on track to record home price growth of at least 6.4% this year.

While that’s good news for property owners, several bank economists think that strong price growth in the housing market is a key factor as to why the RBA won’t cut rates this year.

The international battle against inflation

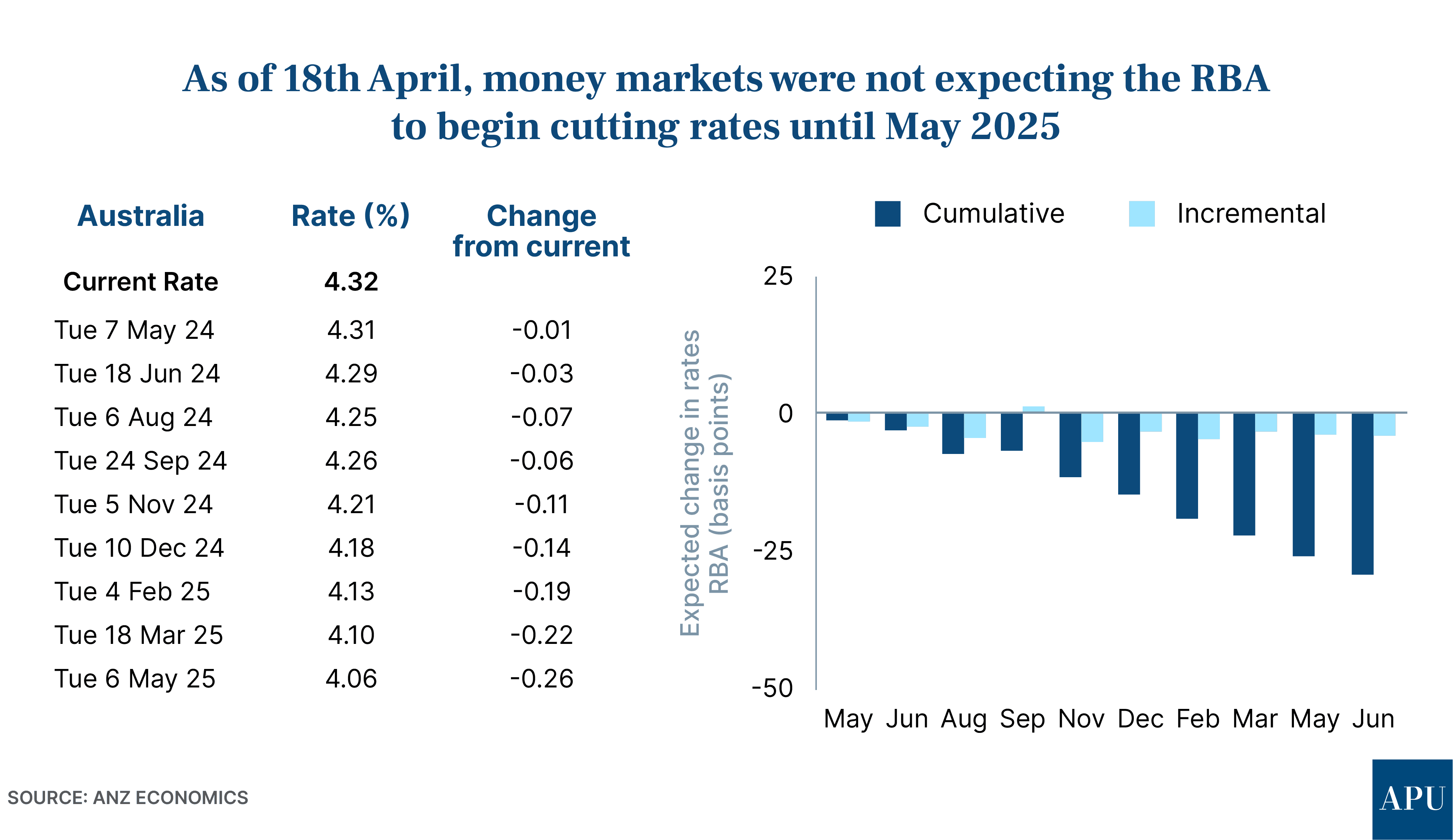

As far as the money markets are concerned, you’re unlikely to see any cut in official interest rates in Australia until mid next year at the earliest.

As of the 18th of April, they’d priced in just one cut of 0.25% by the 6th of May 2025, when the RBA is due to hold its third monetary policy meeting next year.

It’s a far cry from the start of April when markets had priced in at least one full 0.25% cut by about September-November this year and then another by February next year.

So what’s changed?

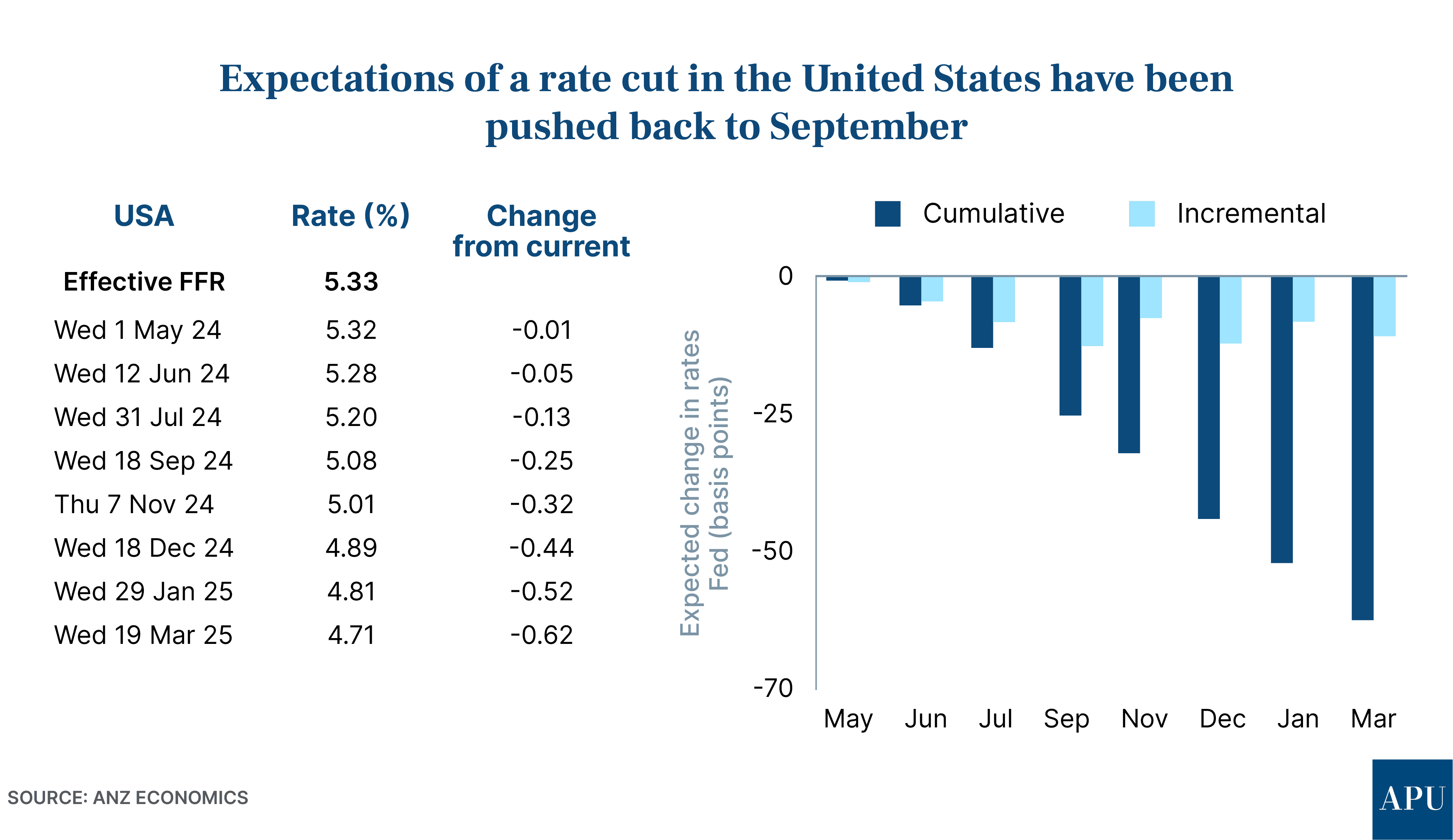

Basically, the money markets have been spooked by stronger-than-expected US inflation figures.

The monthly rise of 0.4% in March means annual inflation in the US is 3.5%, dashing hopes of an early interest rate cut by the Federal Reserve any time soon.

The Federal Reserve’s stated goal is to get America’s inflation rate to near 2% before it even thinks about cutting interest rates.

The Chair of the Federal Reserve, Jerome Powell, could not have been clearer when he recently said that “given the strength in the (US) labour market and progress on inflation so far, it is appropriate to allow restrictive policy (higher interest rates) further time to work.”

Traders pushed back hopes of any rate cuts in the US (America’s effective cash rate is 5.33%) to mid-September.

The way money market traders see implications for Australia goes something like this:

Australia was one of the last advanced economies to begin hiking interest rates after an international outbreak of inflation following the COVID-19 pandemic.

It didn’t raise interest rates as high as many other Western nations, so higher inflation is likely to hang around for longer.

“Monetary policy was less tight in Australia than it was in other countries, and so therefore, the disinflationary impetus coming from the monetary policy has been less,” is the way former RBA official Jonathan Kearns explains this in economist-speak.

However, several leading Australian economists think that logic is flawed, largely because of the so-called “transmission” effects of official interest rates in Australia.

Around 70% of the one-third of Australians with a mortgage are on a variable interest rate - one of the highest proportions in the world.

In the US, it’s around 5%—so when interest rates are jacked up quickly there—very few homeowners are affected, as most people purchase houses on long-term fixed low rates.

AMP Chief Economist Shane Oliver cites that as one of the main reasons he is still expecting the RBA to start cutting rates in August or September this year.

Westpac Chief Economist Luci Ellis - who was an Assistant Governor at the Reserve Bank until late last year - agrees.

“Together with the fact that average mortgage rates paid have risen far less in the United States, macro policy is barely touching the sides for the US consumer,” she says.

She’s sticking by Westpac’s prediction for rate cuts to start here in September.

The higher home price conundrum

On the other side of the fence sit Bendigo Bank’s David Robertson and HSBC’s Paul Bloxham.

Mr Robertson, the chief economist at Australia’s fifth largest bank, does not expect any rate cuts until next year.

“The two scenarios that appear most likely to support early RBA rate cuts by Spring are: a sharp rise in unemployment (as the economy weakens) or a faster than expected fall in core inflation, however an unemployment rate in the threes isn’t consistent with either of these,” Mr Robertson says.

The latest seasonally adjusted figures from the Australian Bureau of Statistics show that the unemployment rate in March rose slightly to 3.8%, but observers say this is likely to mean the RBA’s expectation of around 4.2% unemployment for the June quarter of 2024 is unlikely to be met.

David Roberston also points to the strength of the Australian housing market.

“Another challenge for those forecasting early RBA cuts is persistently high property prices, with the latest CoreLogic data showing another 0.6% rise nationally in March.

“While these findings primarily reflect a lack of new dwellings keeping pace with population growth, it still adds to inflationary risks, so our long-held view that RBA rate cuts are most likely to commence in 2025 remains unchanged,” he says.

HSBC’s Paul Bloxham is in furious agreement about home prices, saying the RBA would not want to add fuel to a hot housing market.

“Although some households have come under pressure from higher interest rates, which has boosted listings, housing demand still appears to be strong relative to supply,” Mr Bloxham says.

“Expectations for rate cuts are also fuelling rising housing prices.

“However, the twist in this story is that the more and faster that housing prices rise, the less likely it is that the RBA will cut rates anytime soon,” he says.

The take out

No matter who is right, the simple fact is that if you were waiting for cheaper interest rates to purchase a property, you risk waiting a very long time.

For those expecting a return to the 2% mortgage rates we saw during the pandemic when the official cash rate was around 0.1%, forget it.

Instead, you need to get used to official interest rates in the 3.5 to 4.5% range, which usually means average retail variable mortgage rates are between the 5 to 7% range.

Basically, expect rates to return to their historical average.

According to Trading Economics, the RBA’s official cash rate was an average of 3.85% between 1990 and 2024.

The good news is that while the fight against inflation is not over, no one is seriously suggesting at this stage that the RBA needs to push interest rates higher again.

The consensus is that the central bank’s unprecedented campaign of 13 interest rate hikes since May 2022 is working—the difference comes when considering how long the effects of those rises will take to percolate through the economy to bring inflation back down to the RBA’s 2-3% target band.

And while Australian residential property may appear expensive at the moment, and prices are still rising, the hard truth is that the property you have your eye on is unlikely to get any cheaper than it is today.

%20Scott%20Kuru%20DPU%20248.jpg?width=1920&height=1080&name=Major%20Banks%20CAUGHT%20Preparing%20For%20Australia%E2%80%99s%20Biggest%20Housing%20Crash%20(Defaults%20%26%20Bankruptcies%20Coming)%20Scott%20Kuru%20DPU%20248.jpg)

%20Scott%20Kuru%20DPU%20247.jpg?width=1920&height=1080&name=This%20Is%20How%20Australia%20Gets%20Pushed%20Into%20the%20Next%20Big%20Reset%20(Trust%20Collapse%20Has%20Officially%20Begun)%20Scott%20Kuru%20DPU%20247.jpg)

%20Scott%20Kuru%20DPU%20239.jpg?width=1920&height=1080&name=URGENT%20Life%20In%20Australia%20Has%20Become%20Impossible%20For%20Millions%20Of%20Aussies%20(It%E2%80%99s%20About%20To%20Get%20Worse)%20Scott%20Kuru%20DPU%20239.jpg)

%20Scott%20Kuru%20DPU%20227.jpg?width=1920&height=1080&name=URGENT%20ALERT%20Australia%E2%80%99s%20Property%20Market%20Is%20Sliding%20Into%20Something%20Much%20Bigger%20(Prepare%20Now)%20Scott%20Kuru%20DPU%20227.jpg)

%20Scott%20Kuru%20DPU%20221.jpg?width=1920&height=1080&name=The%20AI%20Situation%20in%20Australia%20Just%20Hit%20a%20Point%20of%20No%20Return...%20(Major%20Bank%20Proves%20It)%20Scott%20Kuru%20DPU%20221.jpg)

%20Scott%20Kuru%20DPU%20218.jpg?width=1920&height=1080&name=URGENT%20Australia%E2%80%99s%20Diesel%20Supply%20Is%20Far%20Worse%20Than%20People%20Realise%20(Major%20Bank%20Warns)%20Scott%20Kuru%20DPU%20218.jpg)

%20Scott%20Kuru%20DPU%20216.jpg?width=1920&height=1080&name=This%20Is%20How%20Recessions%20Start%20Aussies%20Are%20Shutting%20Their%20Wallets%20(Prepare%20Now)%20Scott%20Kuru%20DPU%20216.jpg)

%20Scott%20Kuru%20DPU%20213.jpg?width=1920&height=1080&name=BREAKING%20Australia%E2%80%99s%20Govt%20Just%20Got%20Caught%20(The%2047%25%20%E2%80%9CPartner%E2%80%9D%20Tax%20Grab)%20Scott%20Kuru%20DPU%20213.jpg)

%20Scott%20Kuru%20DPU%20203.jpg.jpg?width=1920&height=1080&name=Australia%E2%80%99s%20Housing%20Crisis%20Just%20Flipped%20Again%20(BIGGEST%20MARKET%20CRASH%20COMING)%20Scott%20Kuru%20DPU%20203.jpg.jpg)

%20Scott%20Kuru%20DPU%20200.jpg?width=1920&height=1080&name=The%20Govt%E2%80%99s%20Biggest%20Money%20Grab%20The%20Average%20Aussie%20Is%20Getting%20Crushed%20(And%20It%E2%80%99s%20Getting%20Worse)%20Scott%20Kuru%20DPU%20200.jpg)

%20Scott%20Kuru%20DPU%20198.jpg?width=1920&height=1080&name=Farmers%20Panic%20as%20Fuel%20Crisis%20Takes%20Over%20Australia%E2%80%99s%20Fertiliser%20Supply%20(Food%20Shock%20Has%20Begun)%20Scott%20Kuru%20DPU%20198.jpg)

%20Scott%20Kuru%20DPU%20197.jpg?width=1920&height=1080&name=URGENT%20Australia%E2%80%99s%20Property%20Market%20Is%20One%20Rate%20Hike%20Away%20From%20Snapping%20(This%20Is%20How%20It%20Starts)%20Scott%20Kuru%20DPU%20197.jpg)

%20Scott%20Kuru%20DPU%20195.jpg?width=1920&height=1080&name=The%20Biggest%20$83Bn%20Housing%20Scam%20Just%20Got%20Exposed%20(They%E2%80%99re%20Addicted%20to%20Taxing%20the%20Everyday%20Aussie)%20Scott%20Kuru%20DPU%20195.jpg)

%20Scott%20Kuru%20DPU%20192.jpg?width=1920&height=1080&name=The%20Middle%20Class%20Is%20Getting%20Wiped%20Out%20of%20Housing%20(Even%20When%20They%20Do%20Everything%20Right)%20Scott%20Kuru%20DPU%20192.jpg)