.png?width=292&height=292&name=Copy%20Link%20(1).png)

SIGN UP FOR FREE NEWSLETTER

SIGN UP FOR FREE NEWSLETTER

Three new data sets provide evidence that some of the enormous challenges facing the residential construction industry may be easing, but not at a sufficient pace to alleviate the current housing crisis or meet the National Housing Accord targets to build 1.2 million “well-located and affordable” homes by mid-2029.

ABS Building Activity Figures

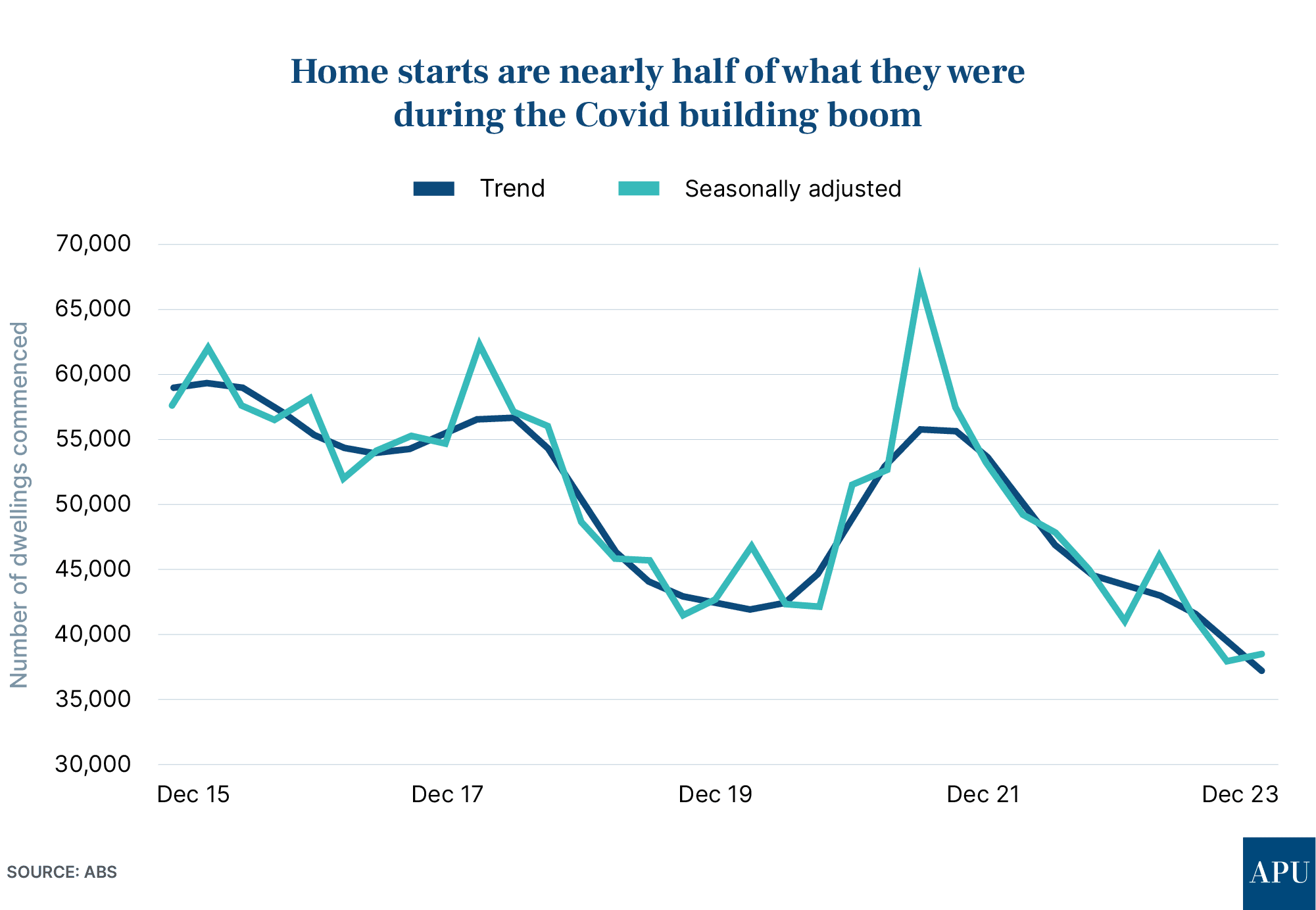

Data from the Australian Bureau of Statistics (ABS) shows dwelling commencements rose 1.3% to 38,397 dwellings during the December quarter of last year.

Work on new houses rose 3.0% but starts on new unit and townhouse developments—exactly the sort of higher-density housing Australian cities need to address the current shortfall—actually fell 2.7%.

In another telling sign, the value of total building work done fell 1.0% to $34.2 billion.

Master Builders Chief Economist Shane Garrett says the ABS figures show that work started on just 163,285 new homes during 2023, a 10.5% reduction on the previous year.

“During 2023, detached house starts dropped by 16.4% to 99,443.”

“This is the lowest in a decade,” Mr. Garrett says.

“The final three months of the 2023 quarter saw higher density home (apartments and townhouse development) starts drop for the third consecutive quarter.”

“A total of 62,720 higher density homes were commenced during 2023 overall - the worst performance in 12 years,” he says.

Antipodean Macro’s Justin Fabo says the dwelling start figures are “well short of what is needed” if the federal government is to have any hope of meeting the National Housing Accord target of building 1.2 million homes over five years from July 1st this year.

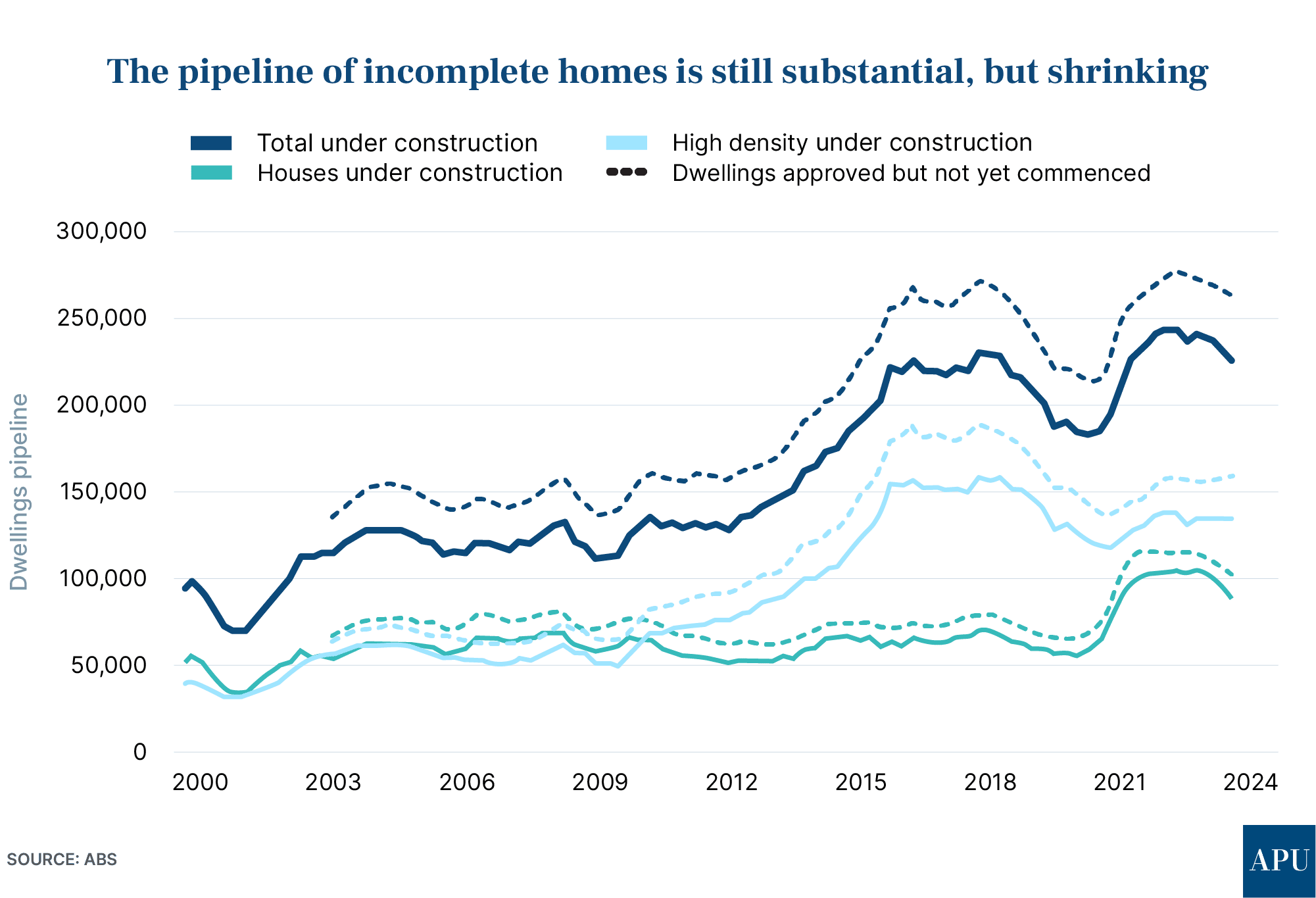

However, the former Treasury official, central banker, and economist points out that dwelling completions “are likely to hold up in the near-term, given the significant ‘excess’ starts in recent years.”

“For detached houses, the number of completions has picked up in recent quarters,” Mr. Fabo says.

Justin Fabo has produced the graph below to show there was still a large pipeline of incomplete dwellings in Australia at the end of 2023, but he says “that pipeline is shrinking.”

Master Builders’ Shane Garrett says the current mismatch between the supply of new properties that can be rented out and the demand for rental accommodation is “particularly worrying”.

“Rental inflation continues to accelerate at a time when price pressures across the rest of the economy have been abating,” Mr Garrett says.

Master Builders Australia Forecasts

Over the longer term, Master Builders Australia appears to be confident that the building and construction industry can better address the shortage of new housing.

The building lobby group has just released its 2024 building and construction industry forecasts.

For the first time, these contain projections of the outlook to mid-2029, which covers the entire five-year period of the National Housing Accord.

The figures clearly show that in at least two financial years – 2027-28 and 2028-29 – the industry will have ramped up enough capacity to build at least 240,000 new homes.

That’s the average number of homes that need to be built each year over the next five years to meet the 1.2 million new homes target.

“We’re seeing inflation starting to near its target range and expect a fall in interest rates which will lead to a more favourable investment market,” says Master Builders CEO Denita Wawn.

“The Federal Government has also announced a number of significant housing measures that focus on increasing supply in social and affordable housing and the rental market.”

But the Master Builders forecast still falls 112,675 homes short of the national target, forecasting there will be 1,087,325 housing starts between 1st July 2024 and 30th June 2029.

Denita Wawn singles out workforce shortages as the number one challenge facing the building industry.

“Constraints on the supply side like workforce shortages, industrial relations changes and a poor planning system counter the full effectiveness of (the government’s) measures,” she says.

.png?width=831&height=553&name=comparison_Apr12_2024%20(2).png)

The Cordell Construction Index

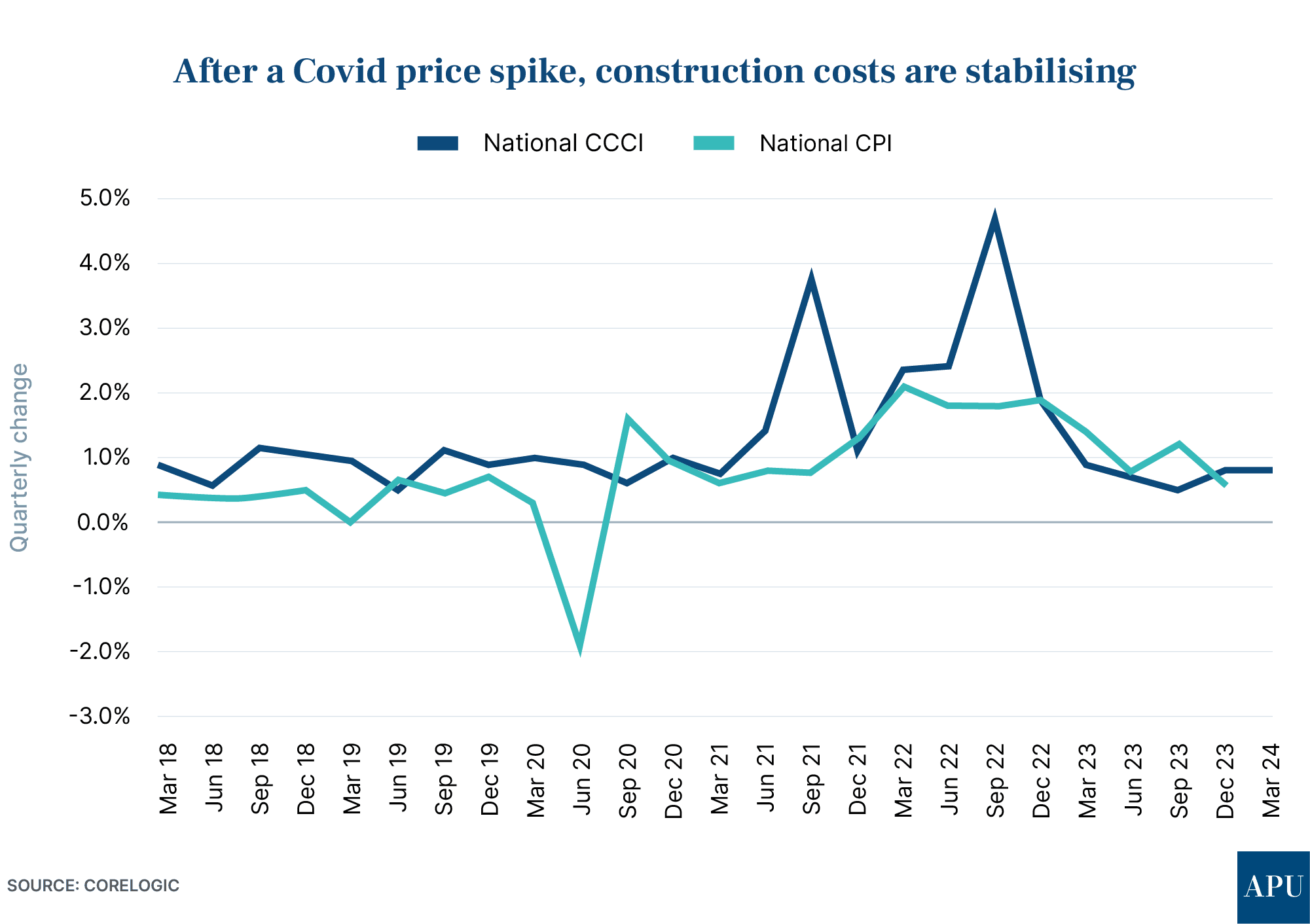

In some much needed good news for builders - especially those locked into fixed-price contracts - CoreLogic’s Cordell Construction Cost Index (CCCI) has recorded that national construction costs rose 0.8% over the March quarter of this year.

That’s the same as the 0.8% rise over the December quarter last year.

While it’s still a rise, the annualised figure of 2.8% is substantially below the 11.9% peak recorded through the 2022 calendar year.

In fact, it’s the smallest annual rise in the national CCCI since the year to March 2007 (2.7%) and well below the pre-COVID decade average (4.0%).

The Cordell Construction Cost Index is an interesting measure, as it’s based on the input costs of building a standard Australian three-bedroom, two-bathroom domestic dwelling.

While construction costs are now roughly back to tracking inflation in trend terms, CoreLogic says it’s important to note that “construction costs aren’t reducing.”

That implies “builder profit margins remain compressed and residential project feasibilities are hard to stack up, following a 27.6% rise in construction costs over the past four years.”

The take-out

One thing is very clear from these three pieces of data.

It’s a challenging time for the residential building industry, and that will continue to be the case in the foreseeable future.

While there’s some optimism that the industry may be able to ramp up the rate at which it builds new homes over the longer term, there’s likely to be a housing shortage in Australia well into the 2030s.

%20Scott%20Kuru%20DPU%20248.jpg?width=1920&height=1080&name=Major%20Banks%20CAUGHT%20Preparing%20For%20Australia%E2%80%99s%20Biggest%20Housing%20Crash%20(Defaults%20%26%20Bankruptcies%20Coming)%20Scott%20Kuru%20DPU%20248.jpg)

%20Scott%20Kuru%20DPU%20247.jpg?width=1920&height=1080&name=This%20Is%20How%20Australia%20Gets%20Pushed%20Into%20the%20Next%20Big%20Reset%20(Trust%20Collapse%20Has%20Officially%20Begun)%20Scott%20Kuru%20DPU%20247.jpg)

%20Scott%20Kuru%20DPU%20239.jpg?width=1920&height=1080&name=URGENT%20Life%20In%20Australia%20Has%20Become%20Impossible%20For%20Millions%20Of%20Aussies%20(It%E2%80%99s%20About%20To%20Get%20Worse)%20Scott%20Kuru%20DPU%20239.jpg)

%20Scott%20Kuru%20DPU%20227.jpg?width=1920&height=1080&name=URGENT%20ALERT%20Australia%E2%80%99s%20Property%20Market%20Is%20Sliding%20Into%20Something%20Much%20Bigger%20(Prepare%20Now)%20Scott%20Kuru%20DPU%20227.jpg)

%20Scott%20Kuru%20DPU%20221.jpg?width=1920&height=1080&name=The%20AI%20Situation%20in%20Australia%20Just%20Hit%20a%20Point%20of%20No%20Return...%20(Major%20Bank%20Proves%20It)%20Scott%20Kuru%20DPU%20221.jpg)

%20Scott%20Kuru%20DPU%20218.jpg?width=1920&height=1080&name=URGENT%20Australia%E2%80%99s%20Diesel%20Supply%20Is%20Far%20Worse%20Than%20People%20Realise%20(Major%20Bank%20Warns)%20Scott%20Kuru%20DPU%20218.jpg)

%20Scott%20Kuru%20DPU%20216.jpg?width=1920&height=1080&name=This%20Is%20How%20Recessions%20Start%20Aussies%20Are%20Shutting%20Their%20Wallets%20(Prepare%20Now)%20Scott%20Kuru%20DPU%20216.jpg)

%20Scott%20Kuru%20DPU%20213.jpg?width=1920&height=1080&name=BREAKING%20Australia%E2%80%99s%20Govt%20Just%20Got%20Caught%20(The%2047%25%20%E2%80%9CPartner%E2%80%9D%20Tax%20Grab)%20Scott%20Kuru%20DPU%20213.jpg)

%20Scott%20Kuru%20DPU%20203.jpg.jpg?width=1920&height=1080&name=Australia%E2%80%99s%20Housing%20Crisis%20Just%20Flipped%20Again%20(BIGGEST%20MARKET%20CRASH%20COMING)%20Scott%20Kuru%20DPU%20203.jpg.jpg)

%20Scott%20Kuru%20DPU%20200.jpg?width=1920&height=1080&name=The%20Govt%E2%80%99s%20Biggest%20Money%20Grab%20The%20Average%20Aussie%20Is%20Getting%20Crushed%20(And%20It%E2%80%99s%20Getting%20Worse)%20Scott%20Kuru%20DPU%20200.jpg)

%20Scott%20Kuru%20DPU%20198.jpg?width=1920&height=1080&name=Farmers%20Panic%20as%20Fuel%20Crisis%20Takes%20Over%20Australia%E2%80%99s%20Fertiliser%20Supply%20(Food%20Shock%20Has%20Begun)%20Scott%20Kuru%20DPU%20198.jpg)

%20Scott%20Kuru%20DPU%20197.jpg?width=1920&height=1080&name=URGENT%20Australia%E2%80%99s%20Property%20Market%20Is%20One%20Rate%20Hike%20Away%20From%20Snapping%20(This%20Is%20How%20It%20Starts)%20Scott%20Kuru%20DPU%20197.jpg)

%20Scott%20Kuru%20DPU%20195.jpg?width=1920&height=1080&name=The%20Biggest%20$83Bn%20Housing%20Scam%20Just%20Got%20Exposed%20(They%E2%80%99re%20Addicted%20to%20Taxing%20the%20Everyday%20Aussie)%20Scott%20Kuru%20DPU%20195.jpg)

%20Scott%20Kuru%20DPU%20192.jpg?width=1920&height=1080&name=The%20Middle%20Class%20Is%20Getting%20Wiped%20Out%20of%20Housing%20(Even%20When%20They%20Do%20Everything%20Right)%20Scott%20Kuru%20DPU%20192.jpg)